Whole Life Insurance Guide 2026: Cost, Cash Value

Last Reviewed: June 2026 | By Sharon O’Day, Senior Advisor | Fact-checked by the Grandfolk Editorial Team

Whole life insurance is the oldest and most straightforward form of permanent coverage: as long as you pay the premiums, it lasts your entire life and pays a guaranteed death benefit whenever that day comes. That permanence is the appeal – unlike term life insurance, you can’t outlive it. The trade-off is cost: whole life typically runs 5 to 15 times the price of comparable term coverage, because part of every premium funds a savings component called cash value. Whether that trade-off is worth it depends entirely on what you’re trying to accomplish.

What is whole life insurance?

Whole life is permanent insurance with three guarantees: a level premium that never rises, a death benefit that never shrinks (as long as premiums are paid), and a cash value that grows at a guaranteed minimum rate. The premium is deliberately set higher than the true cost of insuring you in the early years; those overpayments are invested, and the accumulated balance becomes cash value you can borrow against or withdraw. Because the insurer is on the hook for your whole life, premiums are much higher than term – but they buy certainty.

Types of permanent life insurance

Originally only term and whole life existed. The 1980s and ’90s added several permanent variations:

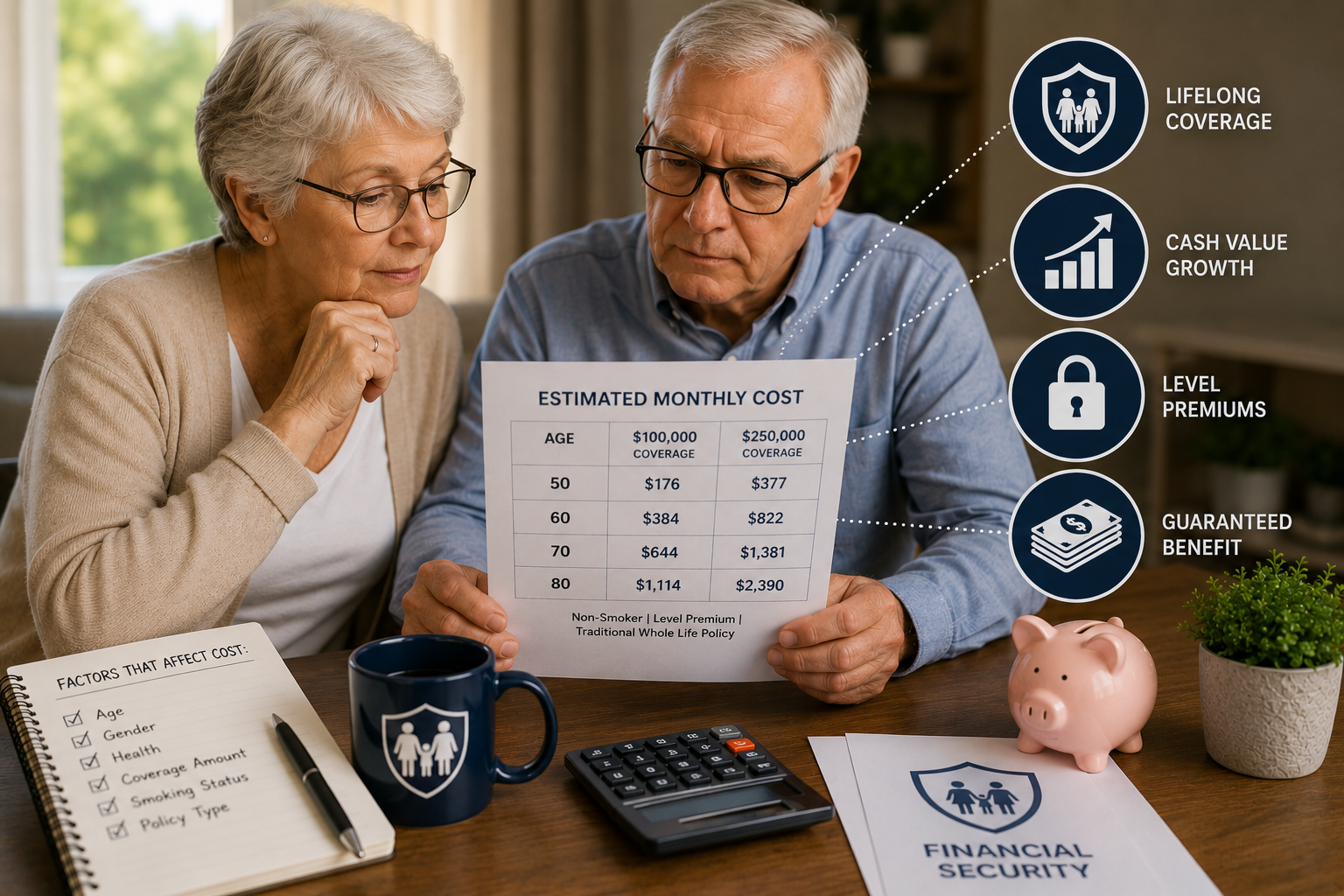

Traditional whole life

Both the death benefit and premium stay level for life. Cash value grows at a guaranteed minimum rate, and with a participating (dividend-paying) policy from a mutual insurer, you may also receive non-guaranteed dividends you can take as cash, use to reduce premiums, or reinvest as paid-up additions that grow coverage.

Universal life (UL)

A flexible-premium permanent policy. Cash value earns interest (often near money-market rates), and you can adjust your premium and death benefit within limits. The flexibility is useful – but if you underfund it, the policy can lapse, so it needs monitoring.

Variable life (VL)

Cash value is invested in stock, bond, and money-market subaccounts. Upside is higher, but so is risk – poor performance can lower both cash value and death benefit, though some policies guarantee a minimum death benefit.

Variable universal life (VUL)

Combines variable life’s investment options with universal life’s premium and death-benefit flexibility – the most flexible and the most complex, with the most risk.

Guaranteed universal life (GUL)

Increasingly the senior favorite. GUL costs a bit more than term but less than whole life, because it builds little or no cash value. Its appeal: you can set coverage to last to a chosen age (often 90–120), so the policy outlives you – unlike term, which usually caps around 80–90. Read the fine print to confirm there are no hidden requirements to keep premiums level.

How cash value and dividends work

Cash value grows tax-deferred and gives you flexibility while you’re alive: you can borrow against it, withdraw from it, use it to cover premiums, or surrender the policy for its cash (surrender) value. Two things to understand clearly:

- Loans reduce the death benefit. If you borrow and die with the loan outstanding, the balance plus interest is subtracted from what your beneficiaries receive.

- With most traditional whole life, beneficiaries receive the death benefit, not the death benefit plus cash value. The insurer effectively retains the cash value at death – it served as your living flexibility, not an extra payout.

Whole life vs. term life: which makes sense for a senior?

| Term life | Whole life (permanent) | |

|---|---|---|

| Duration | Set period (10–30 yrs); can age out | Lifelong |

| Cost | Lowest | 5–15× term |

| Cash value | None | Yes, grows tax-deferred |

| Best for | A temporary need (mortgage, income gap) | Lifelong coverage, a guaranteed legacy, estate liquidity |

If your need is temporary and budget is the priority, term usually wins. If you want coverage that’s guaranteed to pay out whenever you die – for estate taxes, a special-needs dependent, or a legacy – permanent coverage earns its higher cost. For small needs like funeral costs, a final expense / funeral insurance policy (a small guaranteed-acceptance whole-life policy, typically with a two-year graded waiting period) may be all you need.

How much does whole life insurance cost?

Whole life is priced per the face amount, your age, health, and gender, and there’s no single number – but to set expectations:

- A small whole-life / final-expense policy of about $15,000 commonly runs roughly $48–$63/month at age 60 and $78–$103/month at age 70 for a non-smoker (women toward the lower end, men the higher).

- Larger whole-life policies (say $100,000+) cost substantially more – often several hundred dollars a month at senior ages – which is why whole life ends up at 5–15× the cost of comparable term.

- Smokers pay dramatically more, and rates rise sharply with each year of age.

The only number that matters is a real, fully-underwritten quote for your situation – preliminary quotes always assume the best-case rate class.

How underwriting works (medical exam, simplified, guaranteed issue)

Underwriting sets your price based on health and risk:

- Fully underwritten (medical exam): usually the lowest premiums if you’re in reasonable health – the insurer prices on facts, not the unknown. Larger face values almost always require it. The exam typically covers height, weight, blood pressure, and blood/urine tests; applicants over 50 may need an EKG or stress test, and men may be asked for a PSA test.

- Simplified issue (health questions, no exam): faster, higher cost.

- Guaranteed issue (no questions): easiest approval, highest cost per dollar, small face value, two-year graded waiting period.

Don’t reflexively avoid the exam – for healthy applicants it often produces the cheapest coverage. And answer honestly: misstatements can lead to a denied claim within the two-year contestability window.

Riders worth considering

- Living-benefits riders – access part of the death benefit while alive: a terminal illness rider, a long-term care rider (see long-term care insurance), and a critical illness rider.

- Disability waiver of premium – keeps the policy in force if you become disabled.

- Term rider – adds temporary coverage at lower cost.

- Guaranteed insurability / additional purchase option – buy more coverage later without proving insurability.

- Cost-of-living rider – increases coverage to offset inflation.

- Accidental death benefit – pays extra if death results from an accident.

How to choose a policy and vet the insurer

Start with five or six candidate companies and narrow to two or three after comparing full (not just preliminary) quotes on identical coverage. Because you’ll likely hold this policy for the rest of your life, the insurer’s durability matters enormously:

- Check the financial strength rating at A.M. Best – experts suggest at least an A (Excellent), and a Comdex score of 90+.

- Review customer satisfaction in the J.D. Power life insurance study.

- Look up complaints through the NAIC (a complaint ratio near zero is best; the national median is 1).

Whole-life pricing is regulated at the state level, so true differences come from rate class and each company’s expenses and investment performance – another reason to compare full quotes. An independent (multi-line) agent can shop many insurers; a captive agent represents one. Few discounts exist beyond payment mechanics (annual vs. monthly, automatic deduction).

Is whole life insurance worth it? (pros and cons)

Pros

- Lifelong coverage you can’t outlive.

- Level premiums and a guaranteed death benefit.

- Tax-deferred cash value you can borrow against.

- Useful for estate liquidity, special-needs dependents, and guaranteed legacies.

Cons

- Far more expensive than term – many people are better served buying term and investing the difference.

- Cash value grows slowly in early years; surrender charges can make early exits costly.

- Beneficiaries usually receive the death benefit only, not the cash value too.

- Complex products (UL/VUL especially) require ongoing attention.

If you no longer need or can afford a policy, you can surrender it for the cash value or, in some cases, sell it via a life settlement – but either way you give up the death benefit that was the original point.

Whole life insurance providers to compare

Several mutual and stock insurers are commonly compared for permanent coverage. Get full quotes from a few and compare actual terms rather than relying on a generic ranking:

- Northwestern Mutual, MassMutual, New York Life – large mutual insurers known for dividend-paying whole life.

- Mutual of Omaha – widely available, including simplified and guaranteed-issue final-expense whole life.

- State Farm, Principal, Guardian, Pacific Life – other commonly compared options across whole/universal lines.

Frequently asked questions

How much does whole life insurance cost for a 60-year-old?

A small $15,000 final-expense whole-life policy might run about $48–$63/month at 60; larger whole-life policies cost substantially more. Whole life generally costs 5–15 times comparable term coverage.

How does cash value work in whole life insurance?

Part of each premium funds a cash-value account that grows tax-deferred at a guaranteed minimum rate. You can borrow against it or withdraw from it while alive, but loans reduce the death benefit, and with most policies the insurer retains the cash value at death.

Is whole life insurance worth it?

It’s worth it if you want guaranteed lifelong coverage, estate liquidity, or a legacy and can afford the premium long term. For a temporary need on a budget, term is usually the better value.

What happens to the cash value when I die?

With most traditional whole-life policies, beneficiaries receive the death benefit, not the death benefit plus cash value – the insurer effectively keeps the cash value. Some policies or riders pay both at a higher premium.

What’s the difference between whole life and guaranteed universal life (GUL)?

Whole life builds cash value and costs more; GUL builds little or no cash value and costs less, while still providing permanent coverage to a chosen age (often 90–120).

Can I cash out a whole life policy?

Yes. You can surrender it for the cash (surrender) value, though early surrender charges may apply, or you may be able to sell it through a life settlement – both forfeit the death benefit.

Do I need a medical exam for whole life insurance?

For larger face values, usually yes – and a full exam often yields the lowest premium. Simplified-issue (health questions only) and guaranteed-issue (no questions) options exist for smaller policies at a higher cost.

Final thoughts

Whole life insurance buys certainty: lifelong coverage, a guaranteed payout, and a tax-deferred cash value – at a premium far above term. It makes sense when you want guaranteed permanence for estate, legacy, or special-needs reasons, and less sense when a temporary need could be covered more cheaply by term. Compare full quotes, insist on a financially strong insurer, and match the policy type to your goal. For the full range of options, see our guide to life insurance for seniors and the rest of our senior insurance guides.

Sharon O'Day - Senior Advisor

Sharon O'Day is the Health editor at Grandfolk, where she commissions and reviews fitness, wellness, and senior-care content for accuracy, clarity, and real-world usefulness. At 60-plus, she writes for older adults from lived experience, testing the advice against the questions she and her peers actually ask. She focuses on guidance that is honest about both the benefits and the limits, and that always points readers back to their own doctor for personal decisions.